Breaking the Bottleneck | Issue 15

[06/5/2023]Factory Construction, Solar Manufacturing, and Q2 NAM Survey

Breaking the Bottleneck is a weekly manufacturing technology newsletter with perspectives, interviews, news, funding announcements, and a startup database. For a high-level market map on discrete and continuous manufacturing click the link here! If you know anyone looking to chat about manufacturing tech, I’d love to talk!

Content I Enjoyed This Week 🏭🗞️🔬

News:

Factory Boom Sweeps US Construction [Bloomberg]

Data from the US Census Bureau reveals that spending on construction by manufacturers has more than doubled in the past year, reaching an annual rate of nearly $190 billion in April. Manufacturing now represents about 13% of all non-government construction, the highest proportion since the early 1990s. This boom in factory construction coincides with a decline in residential construction, as the housing market cools off after a period of high demand during the pandemic.

U.S. Allows Korean, Taiwanese Chip Makers to Keep Chines Operations [WSJ]

The Biden administration is planning to allow top semiconductor manufacturers from South Korea and Taiwan to continue and expand their chip-making operations in China without facing reprisals from the United States. The decision to extend existing exemptions from US export-control policies, which restrict the sale of chips and chip-making equipment to China, has raised concerns among analysts who believe it weakens US efforts to slow China's technological advancement. The exemptions were initially implemented in October 2022 and were set to expire in October 2023. However, the Biden administration intends to renew them indefinitely, signaling recognition of the challenges in isolating China from high-tech goods.

Can the US Manufacture Enough Solar Panels? [Canary Media]

The U.S. solar industry is aiming to reduce its reliance on imported solar panels by scaling up domestic manufacturing, backed by federal incentives. Currently, the U.S. imports most of its solar panels, with a significant portion coming from China. “Until cell manufacturing capacity matches module assembly capacity, imported cells will remain a key part of the panel assembly supply chain.” Even in the best-case scenario, in which manufacturers hit 100 percent of the production timelines and targets they’ve announced, the Solar Energy Industries Association estimates that the U.S. will still need to import 24 gigawatts of solar panels in 2030 alone. The country installed 17 gigawatts last year, for reference. Despite efforts to boost domestic manufacturing, the U.S. still has a long way to go to achieve solar self-sufficiency.

Microsoft’s Supply Chain Holding Back Its Climate Ambitions [The Verge]

Microsoft, Apple, and Google are the only three big tech companies that have achieved 100 percent renewable energy in their direct operations, but the emissions from their supply chains far outweigh their direct emissions. Microsoft in particular has struggled to reduce carbon emissions across its supply chain in alignment with its goal of reaching carbon negativity. The company has faced challenges in ensuring that its suppliers adhere to its climate targets, resulting in increased emissions from the supply chain. The Verge reviewed 27 emissions inventories from Microsoft's top 100 suppliers and found that most of them had increased their emissions and only a few suppliers showed progress in reducing their carbon footprint.

To try and address supply chain and supplier emissions, Microsoft updated its Supplier Code of Conduct to require suppliers to cut carbon emissions by 55 percent by 2030. However, some details remain uncertain, such as whether suppliers can rely on carbon offsets instead of directly replacing fossil fuels with renewables. Experts recommend that Microsoft should enforce stricter regulations and support suppliers in transitioning to 100 percent renewable energy by 2030.

Automakers Are Adopting Tesla’s Gigacasting [Reuters]

Toyota Motor announced its adoption of Tesla's "Gigacasting" technology, aiming to enhance the performance and reduce costs of its future electric vehicles (EVs). Gigacasting refers to the use of large-scale aluminum die-casting machines, known as Giga Presses, which produce aluminum parts bigger than those used in traditional auto manufacturing. This innovation allows for fewer parts, lower costs, simplified production lines, and weight reduction in vehicles. Tesla's profitability has been attributed to the use of Gigacasting, as it enables the consolidation of multiple parts into a single component. Toyota expects to eliminate numerous sheet metal parts and reduce waste by using aluminum die-casting. Other automakers, such as General Motors, Hyundai, and Volvo, are also pursuing Gigacasting technology. However, the cost of investment and potential challenges in repairing cars with single-piece cast bodies remain considerations for legacy automakers.

Research:

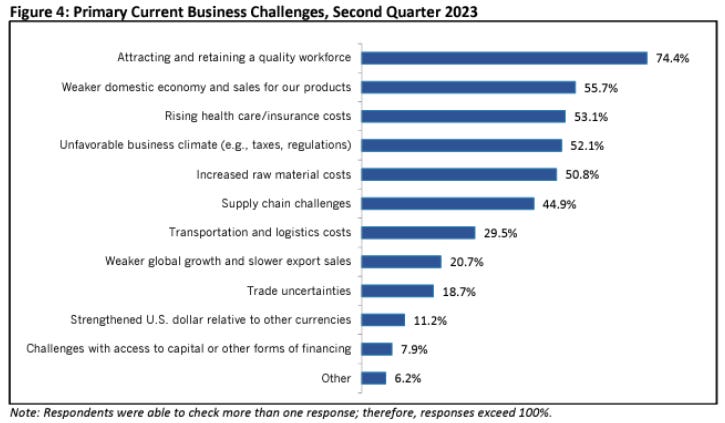

NAM Manufacturer’s Outlook Q2 2023 [NAM]

Manufacturing sentiment in Q2 2023 was the lowest since Q3 2020

More than 74% of manufacturers cited the inability to attract and retain employees as their top primary challenge

Given the tight labor market and changing expectations about work, 57.7% of respondents were exploring scheduling changes—including compressed workweeks, adjusted shift times and split shifts, among other options—to better attract or retain employees.

53% of manufacturers expect improvement in supply chains by year’s end

Podcasts/Video:

EVs in America With GM Sustainability Chief [June 23]

James Dyson [Founders Podcast]

Twitter/Reddit:

Winding Rotors with Electric Motors

Manufacturing Deals

Sparetech - a German based collaboration-platform for manufacturing companies to digitize their inventories of spare parts, calculate their real demand, compare parts from different suppliers and source the appropriate part outside or within their production network

$10 million [Series A] - Led by Insight Partners and Headline

Percepto - an Austin-based drone solution provider to help industrial sites monitor and inspect their critical infrastructure and assets

$50 million [Series C] - Led by Koch Disruptive Technologies and joined by Zimmer Partners, U.S. Venture Partners, Delek US Holdings, Atento Capital, Spider Capital, and Arkin Holdings

Vivolta - a world leader in the development and manufacturing of electrospun medical products

€7 million [Series Seed] - Led by the Dutch government via the NXTGEN HIGHTECH growth fund