Breaking the Bottleneck | Issue 34

[12/11/2023] Scope 3 Emissions, 2023 Capital Spending Survey, AI in Manufacturing & More

Breaking the Bottleneck is a weekly manufacturing technology newsletter with perspectives, interviews, news, funding announcements, and a startup database. For a discrete and continuous manufacturing market map click the link here!

Content I Enjoyed This Week 🏭🗞️🔬

News:

EV Industry Faces A Choice: Tax Credits or Chinese Batteries [Canary Media]

The Biden administration has unveiled proposed guidelines for enforcing the Inflation Reduction Act's electric vehicle (EV) incentives, focusing on reducing reliance on China in the U.S. EV and battery industries. The guidelines aim to address one of the most complex aspects of the legislation, EVs containing battery components from a "foreign entity of concern" will be ineligible for the $7,500 federal tax credit. By 2025, additional restrictions will disqualify EVs that include any critical minerals processed or recycled by such foreign entities. This move seeks to encourage EV manufacturers to secure battery supplies from sources outside of China, prompting calls for policies that accelerate this transition and establish the U.S. as a leader in the entire EV battery industry. However, the challenge lies in the practicality of securing alternative sources for minerals and components outside China's dominant position in the global EV supply chain. While U.S. companies, along with European and Asian partners, are rapidly expanding domestic EV and battery manufacturing capacity, they still heavily rely on supply chains controlled by Chinese firms. The proposed rules could complicate existing cooperative ventures between U.S. and Chinese companies in battery manufacturing, materials processing, and mining. The guidelines scrutinize joint ventures, licensing agreements, and other collaborations with companies from the listed countries, potentially rendering resulting products ineligible for the tax credit.

The Manufacturing Shift Is Affecting Shipping [QZ]

The global shipping industry faces collapsing container rates, a freight recession, and overcapacity. However, intra-Asia shipping is a bright spot, driven by manufacturers diversifying their supply chains. Vietnam, in particular, has become a critical node in global trade flows due to surging foreign investment and increased manufacturing activity. Direct shipping routes between Vietnam and the US have almost doubled, and Vietnam's ranking in countries with direct shipping services to the US has sharply risen. The country's maritime transport industry is experiencing remarkable growth, with an 83% increase in scheduled deployed capacity between the US and Vietnam from 2019 to 2023. While China remains central to global trade, the trend of diversification is evident as Vietnam becomes an extra call in shipping routes, confirming Asia's role as the manufacturer of the world. For Vietnam to fully capitalize on increased intra-Asia shipping, infrastructure investment, possibly from China, is essential to enhance port efficiency and connectivity. China has shown interest in port investments across Asia, viewing it as a form of "port diplomacy" to gain global leverage.

Looking to Maintenance to Boost Semiconductor Efficiency [McKinsey]

The global semiconductor industry is expected to grow at 6 to 8 percent per year through 2030, reaching $1 trillion in annual revenue with 40% of it being driven by industries requiring mature nodes, such as automotive, industrial, and wired communication. The aging facilities responsible for mature node manufacturing, known as fabs, are facing challenges in meeting increased demand and minimizing maintenance-related downtime. Improving equipment reliability can enhance tool availability by more than 15 percent, contributing to an overall equipment effectiveness (OEE) increase of 70 to 80 percent. Fab leaders need to shift from reactive to preventive approaches, focusing on equipment recovery, consistent planned maintenance, and efficient parts management. Best-in-class planned maintenance programs increase fab availability by 5 to 7 percentage points, requiring commitment from top management, accountability, and continuous improvement. Efficient parts management, often overlooked, can significantly impact fab availability, and a control tower approach with real-time data analysis is recommended to address parts-related challenges.

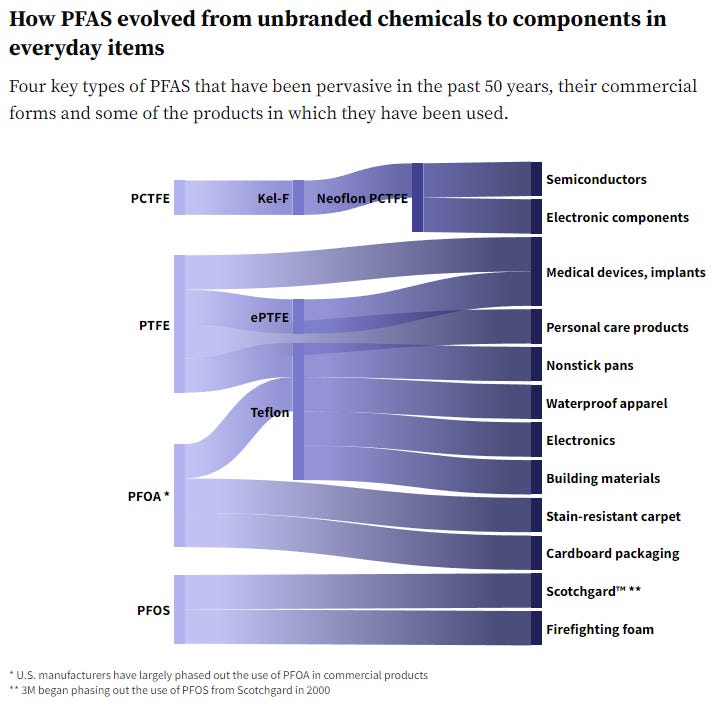

The History of PFAS [Manufacturing Dive]

Polyfluoroalkyl substances (PFAS), are synthetic, fluorine-based chemicals, often referred to as "forever chemicals." The use of PFAS, discovered in the 1930s, went largely unregulated until the early 2000s, and their toxicity, environmental persistence, and health risks were not widely recognized until the late 1990s. PFAS are key components in various products, ranging from medical devices and aircraft to semiconductors, due to their waterproof, durable, and heat-resistant qualities. The evolution of PFAS started with the discovery of polychlorotrifluoroethylene (PCTFE) in 1934, which later became Neoflon PCTFE and is used in semiconductors. Another significant PFAS, Teflon, was discovered accidentally in 1938 and gained popularity for its use in non-stick cookware and various products. DuPont trademarked Teflon in 1945, and it was used in the Manhattan Project during World War II. The Simons Process, developed by Joseph A. Simons, played a crucial role in upscaling the production of PFAS, specifically perfluorooctanoic acid (PFOA), which was used in Teflon production and other applications. DuPont purchased PFOA from 3M to improve its Teflon production process. The post-war period saw the widespread use of PFAS in various industries, leading to unintended consequences and hazards.

What Are Automakers Doing to Cut Scope 1-3 Emissions? [Industry Week]

The automotive industry’s decarbonization strategy includes addressing Scope 3 emissions, such as those from materials production. Ford's new EV plant in Germany exemplifies efforts to reduce emissions in Scopes 1, 2, and 3 by focusing on the main carbon-emitting hotspots in automotive supply chains. These include:

Steel: Traditional steel production emits high carbon, but efforts involve adopting innovative technologies like hydrogen-based steelmaking and renewable-powered electric arc furnaces.

Plastics: Plastics, widely used in vehicles, contribute to emissions. Addressing this involves embracing circular economy principles, recycling, and developing bio-based alternatives.

Aluminum: Traditional aluminum production is energy-intensive, but the adoption of recycled aluminum and low-carbon primary aluminum production is crucial for sustainability.

Batteries: Battery production for electric vehicles (EVs) poses environmental challenges. Efforts focus on improving battery technology, exploring alternatives, and implementing recycling programs to minimize environmental impact.

To do this OEMs like Ford are acquiring information about their suppliers' operations to set production, quality, performance, costs, and ecology benchmarks. Furthermore, they are relying on governments to incentivize collaboration and supplier buy-in throughout the entire value chain of electric batteries, from material mining to end-of-life considerations.

Research:

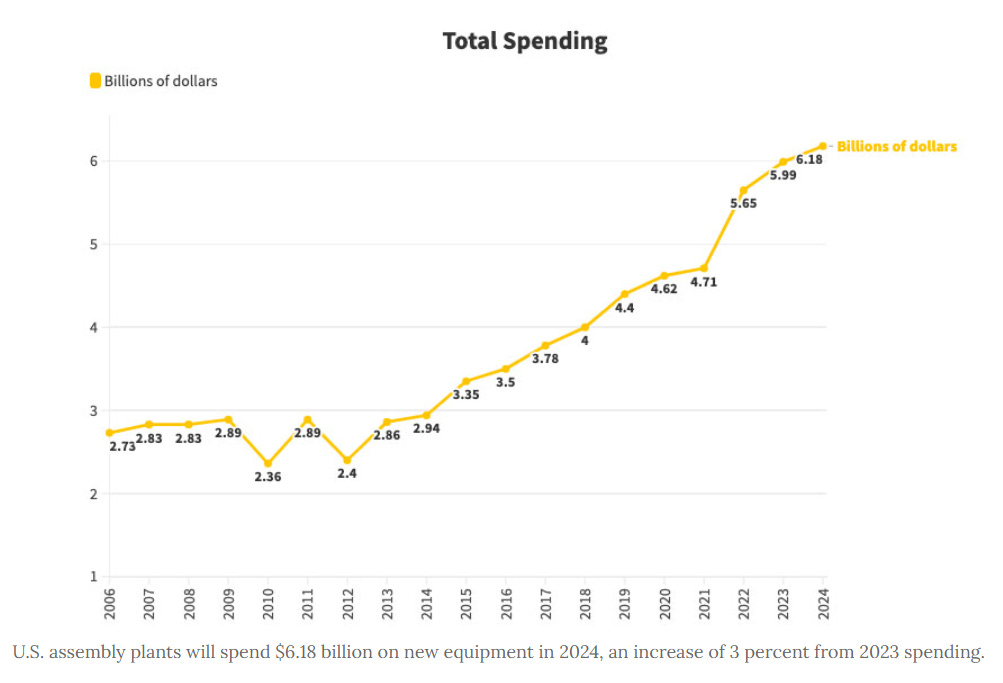

2023 Manufacturing Capital Spending Survey [Assembly Magazine]

Here are some highlights from Assembly Magazine’s 28th Annual Capital Equipment Spending Survey:

U.S. assembly plants will spend $6.18 billion on new equipment in 2024, an increase of 3 percent from the $5.98 billion projected to be spent in 2023.

The Automotive industry will account for 63 percent of all spending next year and automotive assemblers will spend $7,786,111 on capital equipment next year, 4x the national average.

After accounting for more than 30 percent of total equipment spending in each of the past two years, machinery manufacturers (NAIC 333) will represent just 2 percent of spending in 2024.

The Midwest has traditionally been the epicenter of U.S. manufacturing, and next year will be no exception. The region will account for 52 percent of spending in 2024, more than any other part of the country and the most for the region since 2018.

“The world record of 500,000 units was exceeded for the second year in succession,” says Marina Bill, president of IFR and group vice president for robotics and discrete automation at ABB Inc. “In 2023, the industrial robot market is expected to grow by 7 percent to more than 590,000 units worldwide.”

We expect sales of six-axis robots, SCARAs, grippers, and other robotic technology to increase 11 percent, from $720 million in 2023 to $799.4 million in 2024.

DeepMind New Material Discovery AI Tool [Deepmind]

Researchers at Deepmind have developed a new deep learning tool called Graph Networks for Materials Exploration (GNoME), which significantly accelerates the discovery of stable inorganic crystals, essential for various modern technologies. GNoME predicted the stability of 2.2 million new crystals, equivalent to almost 800 years' worth of knowledge. Among these predictions, 380,000 are identified as the most stable, showing promise for experimental synthesis. These materials have potential applications in transformative technologies like superconductors, advanced batteries, and more. The researchers released GNoME's predictions to the research community, contributing 380,000 materials to the Materials Project for further exploration and experimentation. The AI-guided approach has the potential to revolutionize materials discovery at an unprecedented scale and accuracy.

The Economic Downsides of Right to Repair [NAM]

A study commissioned by the National Association of Manufacturers (NAM) suggests that "right-to-repair" policies, which are currently in place in over 30 states, could have negative economic impacts. The study, titled "The Economic Downsides of ‘Right-to-Repair,’” states that such policies might disrupt supply chains, increase the risk of intellectual property theft for manufacturers, raise costs for both consumers and manufacturers and potentially lead to an increase in greenhouse gas emissions. The study argues that these policies could result in unintended and harmful consequences, making product repair more challenging and increasing compliance costs for manufacturers.

Podcasts:

Chart of the Week:

The Development of the Asia Circle & Deglobalization [Hexopedia]

AI in Manufacturing [AI Chat]

Manufacturing Deals

Atomic Industries - An company looking to automate tool and die making

$17 million [Seed] - Led by Narya and joined by 090 Industries, Acequia Capital New Industrials, Porsche Ventures, Yamaha Motor Ventures, Toyota Ventures and Impatient Ventures

Fortellix - A developer of verification and validation solutions for self-driving and ADAS systems

$85 million [Series C] - Led by 83North and joined by Temasek, Toyota's Woven Capital, Nvidia, Artofin and insiders MoreTech, Nationwide, Volvo Group VC, Jump Capital, Next Gear Ventures, and OurCrowd

Gecko Robotics - A company building ultrasonic inspection robots for understanding the current condition of critical infrastructure

$85 million [Series C Extension] - Led by USIT and Founders Fund

Machinery Partner - A company building a platform for manufacturers to purchase equipment from their factories

$11 million [Series A] - From ASV, Pritzker Group, Pacific Western Bank, One Way Ventures, Euclid Group, and Techstars Ventures

MaintainX - A company building the a modern CMMS for manufacturing

$50 million [Series C] - Led by Bain Capital Ventures and joined by Bessemer Venture Partners, Amity Ventures

Weekly Planned Downtime

Barbenheimer Round Two

Jensen Huang on the Future of AI