Breaking the Bottleneck | Issue 54

[7/15/2024] New Manufacturing Market Maps, Digital Twins in IC Design, Industrial Engineering by Schematic Ventures & More!

Breaking the Bottleneck is a weekly manufacturing technology newsletter with perspectives, interviews, news, funding announcements, manufacturing market maps, and a startup database!

💥 Have you seen any exciting startups recently? I’d love to chat with them!

🏭 If you were forwarded this and found it interesting, please sign up!

New Manufacturing Market Maps!!!

Discrete Manufacturing

Process / Continuous Manufacturing

Content I Enjoyed Last Week 🏭🗞️🔬 📚

News:

In a First, A Solar Microgrid Will Power an Industrial Plant [Canary Media]

Timet is constructing a new titanium melting facility in Ravenswood, West Virginia, which is set to operate primarily on renewable energy starting next year. The facility, part of Berkshire Hathaway's Titanium Metals Corporation (Timet), will use a solar microgrid developed by BHE Renewables, also a Berkshire Hathaway company. This setup is pioneering as the project demonstrates the capability of microgrids to meet industrial energy demands efficiently and sustainably. The solar microgrid will include a 106 MW solar array and a 50 MW battery energy storage system designed to provide reliable power required for the titanium melting furnaces. David Dugan of Precision Castparts Corp., Timet's parent company, emphasizes that this setup will offer cost-effective power comparable to traditional sources, which is crucial for energy-intensive titanium production. The project represents a substantial investment, with Timet estimating a total investment of over $500 million for the facility. Innovative approaches like Timet's integration of renewable energy and advancements in titanium production methods, such as hydrogen-assisted metallothermic reduction (HAMR), are poised to reshape the industry. These developments could reduce CO2 emissions significantly compared to conventional methods, making titanium more accessible for broader industrial applications beyond its current high-cost niches.

How to Build EV Motors W/O Rare Earth Elements [IEEE Spectrum]

Currently, most EV motors rely heavily on neodymium iron boron magnets, which are REE-dependent and primarily sourced from China. This reliance poses geopolitical and environmental risks. Efforts are underway globally, particularly in the US and Europe, to develop REE-free motor technologies. These initiatives involve collaborations between government agencies, automakers like General Motors and Tesla, and startups like Niron Magnetics. These entities are exploring alternatives like ferrite magnets, alnico, iron nitride (FeN), and manganese bismuth (MnBi), each with varying trade-offs regarding performance metrics like remanence and coercivity. Researchers at Oak Ridge National Laboratory (ORNL) are driving this research, developing advanced motor designs that minimize or eliminate the need for REEs. Their work includes optimizing motor performance through innovative magnet designs and integrating power electronics within the motor structure to enhance efficiency and reduce weight. New motor designs, such as synchronous motors with electromagnets powered by rotary transformers, are also emerging, offering flexibility in adjusting magnetic fields for efficiency gains across various operating speeds. However, this transition faces challenges, including maintaining performance parity with torque output and demagnetization resistance.

Digital Twins Find Footing in IC Design [Semiconductor Engineering]

Digital twins increasingly gain traction in semiconductor manufacturing, promising significant efficiency, quality, and flexibility improvements across fab and assembly operations. Digital twins are already employed for run-to-run control and lot scheduling in semiconductor manufacturing. These applications aim to optimize processes by modeling interactions between various electrical and physical characteristics, thereby improving overall operational efficiency. Anjaneya Thakar from Synopsys highlights the potential of digital twins to replace costly physical runs with software simulations, enabling faster decision-making and cost savings: "With digital twins, you can get your response to particular real-time information faster and hopefully at a lower cost." This approach leverages real-time data from the fab to enhance process control and operational efficiency. Joseph Ervin from Lam Research also emphasizes the improvements in speed-to-solution and innovation cost reduction: "With virtual materials and equipment, experimentation can be drastically faster, less expensive, more accessible, richer in data, and less costly." Despite these benefits, several challenges hinder widespread adoption. A significant hurdle is the lack of a standardized framework and interface for digital twins in semiconductor manufacturing. Currently, solutions are often developed in silos, complicating interoperability and scalability across different processes and vendors. Standardization efforts are crucial to overcoming these challenges and maximizing the potential of digital twins. To overcome this, Indranil Sircar from Microsoft underscores the importance of starting with small implementations and gradually scaling up to higher levels of complexity and abstraction.

Why Most Battery-Makers Struggle to Make Money [Economist]

The cyclic nature of boom-and-bust cycles occurs across various industries and is now evident in battery manufacturing for electric vehicles (EVs). The sector faces challenges despite over $520 billion invested globally in battery production since 2018, driven by anticipated EV demand. Prices for batteries have decreased, yet not enough to spur widespread EV adoption. Companies like SK On and Northvolt are experiencing difficulties, with the former in "emergency management" and the latter delaying new factories. Uncertainty persists due to fast-evolving technology and unreliable forecasts of EV uptake. Potential solutions include investing in cheaper battery technologies and promoting freer trade to lower costs outside China, where EV adoption rates are higher due to lower battery prices.

Why has US Manufacturing Stagnated? [Noahopinion]

Throughout the 2010s, a prevailing assumption held that manufacturing industries inherently achieved faster productivity growth than service sectors due to their reliance on advancing technology. Historically, this occurred as industries leveraging better machines naturally progressed faster than labor-intensive services. However, this conventional wisdom ceased to hold after 2011, when U.S. manufacturing productivity not only hit a ceiling but began to decline. Joey Politano's analysis underscores this productivity stagnation across various manufacturing industries, illustrating a broader trend. This contrasts sharply with global patterns where other countries, such as Germany and Korea, continued to advance manufacturing productivity. The U.S. and Japan, in particular, exhibited notably poor performance since 2009, as highlighted by Greg Ip's findings in the Op-ed. The initial boost in U.S. manufacturing productivity pre-2011 was primarily driven by the computer and electronics sector, benefiting from Moore's Law. This era saw rapid quality improvements with offshoring to China during the 2000s, which inflated measured productivity due to composition effects and methodological biases in data collection. A pessimistic view suggests that the era of rapid productivity gains from IT-related advancements may have peaked, evidenced by diminishing returns in recent years. This poses a significant challenge for future growth in manufacturing productivity despite ongoing investments in R&D and potential gains from renewable energy and advanced materials. Policy implications will be profound moving forward, and enhancing export competitiveness will emerge as critical, given the comparatively low share of U.S. exports in its GDP compared to other advanced economies.

Research:

Industrial Engineering by Schematic Ventures

Fantastic interview with Ryan Hannon, VP of Industrial Engineering and Collaborative Innovation at Pitney Bowes, as part of Schematic Ventures' new series, focused on navigating technical software decisions within industrial companies. The series will cover everything from optimizing infrastructure choices and leveraging DevOps best practices to harnessing the power of cloud technologies and improving data workflows in supply chain and manufacturing. Contact ananya@schematicventures.com if you’d like to connect and be featured!

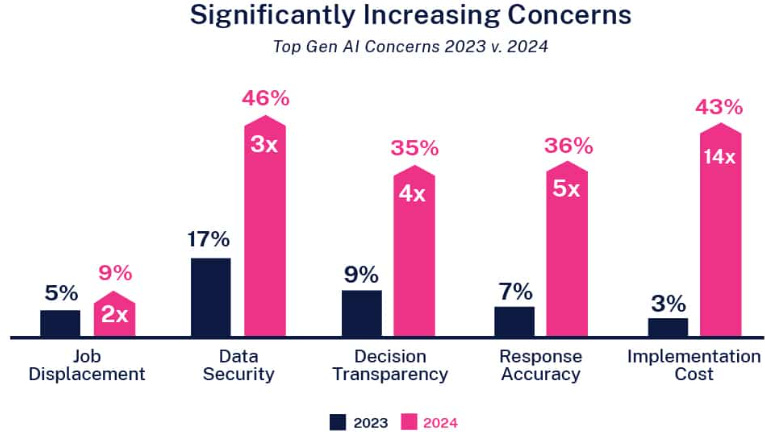

Generative AI Global Benchmark Study [Lucidworks]

The 2024 Generative AI Global Benchmark Study reveals that nearly half of manufacturers already realize cost benefits from their AI initiatives. Other interesting takeaways from the study include:

Less than 60% of manufacturers plan to increase AI spending in 2024 compared to 93% in 2023

44% of manufacturers are concerned with response accuracy

Nearly 70% of manufacturers have experimented with LLMs such as Gemini and Chat GPT, with the remainder opting for open-source models such as LLaMa 3 & Mistral.

Only 1 in 4 companies across all industries have successfully launched AI initiatives in the past 12 months.

Podcasts/Video:

Building Shock Proof Supply Chains [Odd Lots]

Manufacturing Deals🏭💵

Skild AI- A company building general purpose robotic intelligence

$300 million [Series A] - Co-led by Lightspeed Venture Partners, Coatue, SoftBank Group, & Jeff Bezos and joined by Felicis Ventures, Sequoia Capital, Menlo Ventures, General Catalyst, CRV, Amazon, SV Angel, & CMU

X-Bow Systems - A company developing solid rocket motors via additive manufacturing

$70 million [Series B] - Led by Razors Edge and joined by Lockheed Martin Ventures, Boeing Ventures, Crosslink Capital, & Balerion Space Ventures

Armada - An edge computing startup focused on enabling satellite connectivity

$40 million [Venture] - Led by M12 and joined by Founders Fund, Lux Capital, Felicis, Valor Equity Partners, 8VC, & Shield Capital

Jacobi Robotics - A software development platform making industrial arms faster and easier to program

$5 million [Seed] - Led by Moxxie Ventures and joined by Foothill Ventures, Humba Ventures, The House Fund, Swift Ventures, & LDV Partners

Planned Downtime 🏭🧑🔧

Gladiator 2 Trailer