Breaking the Bottleneck | Issue 72

[2/17/2024] Lasers on Silicon, π0, Onshape CAM, & More!

Breaking the Bottleneck is a weekly manufacturing technology newsletter with perspectives, interviews, news, funding announcements, manufacturing market maps, and a startup database!

💥 If you are building, operating, or investing in manufacturing, hardware, or robots, please reach out. My email is aditya@schematicventures.com – I’d love to chat!

🏭 If you were forwarded this and found it interesting, please sign up!

Content I Enjoyed Last Week 🏭🗞️🔬 📚

News:

How to Grow a Laser on Silicon [IEEE Spectrum]

Silicon photonic circuits are essential in data centers, sensors, and autonomous vehicle lidar, but integrating lasers onto silicon chips has remained a significant challenge due to material incompatibilities. Traditional methods involve bonding separate gallium arsenide (GaAs) components onto silicon or transferring pre-made lasers, introducing inefficiencies, alignment difficulties, and material waste. Imec’s nanoridge lasers, which operate at a wavelength of 1,020 nanometers, represent a promising step toward scalable, cost-effective photonic circuits. By embedding indium gallium arsenide layers to control the emission wavelength and integrating electrical contacts and mirrors, the researchers successfully produced hundreds of lasers and photodetectors on full-scale 300-mm wafers, a feat previously unattainable. While the current wavelength is shorter than typical telecommunications standards, efforts are underway to extend it. Additionally, the team is refining the design to mitigate defects near electrical contacts, which currently limit long-term performance. This advancement, highlighted in a recent Nature publication, has been recognized by experts as a potential game-changer for low-cost, mass production of photonic devices, paving the way for more efficient and scalable silicon photonics.

China’s EV Giants Are Betting Big On Humanoids [MIT Technology Review]

China’s EV industry is rapidly expanding into humanoid robotics. The technological crossover between EVs and humanoid robots is fueling innovation. Both fields utilize lidar, depth cameras, and AI-driven navigation, initially designed for autonomous driving, to enhance robotic perception and movement. Battery technology is another shared domain—GAC’s GoMate robot operates on EV-derived battery packs for extended six-hour factory shifts. At the 2025 CCTV New Year Gala, 16 humanoid robots from Unitree performed a synchronized dance, demonstrating China’s advancements in robotics. While Unitree’s H1 robot is already used in EV factories through partnerships with BYD and XPeng, EV manufacturers are now developing their humanoid robots. GAC Group has introduced the GoMate robot for automotive wiring, with plans for mass production by 2026. Nio has formed an in-house R&D team and partnered with UBTech for robotics development. China’s dominance in humanoid-robot supply chains is a crucial advantage; it controls 63% of global suppliers for key components, particularly actuators and rare earth materials, enabling lower production costs. Unitree’s H1 robot costs $90,000, less than half the price of Boston Dynamics’ Atlas. However, China lags in AI and semiconductor technology, where companies like Nvidia, TSMC, and Qualcomm lead the industry. To close this gap, the Chinese government is accelerating automation efforts, with the Robotics+ action plan aiming to double manufacturing robot density by 2025 and provincial R&D subsidies covering up to 30% of project costs. As China’s EV firms pivot toward robotics, the industry is poised to become a trillion yuan market, echoing the rapid rise of the EV sector a decade ago.

Onshape CAM Studio [PTC]

Onshape AI Advisor Is Coming Soon [Engineering.com]

Onshape, PTC’s cloud-based CAD platform, is preparing to launch AI Advisor, an AI-powered chatbot designed to assist users with product support and design guidance. Expected to roll out soon, AI Advisor is powered by Amazon Bedrock and fine-tuned for Onshape users to provide context-specific answers with cited sources, outperforming general AI chatbots like ChatGPT and Perplexity. Initially, it will be a support assistant, answering user queries about modeling techniques, feature recommendations, and best practices. However, future enhancements could enable more advanced capabilities, such as generating expressions, suggesting model optimizations, automating API calls, and even modifying CAD models through text-to-CAD interactions. AI Advisor will launch for all Onshape users, including free and educational tiers, though premium features may later be restricted to higher subscription levels. Beyond AI Advisor, Onshape is developing AI-powered rendering and generative text-to-CAD features. However, the company prioritizes functionality over hype, ensuring that AI tools provide real, professional-grade utility rather than just flashy demos. Jon Hirschtick, Onshape’s founder and PTC’s chief evangelist, emphasized that while generative AI is a promising frontier, Onshape focuses on creating AI-driven tools that professionals will find reliable and valuable for real-world engineering workflows.

The Conglomerate Model Works Very Well – Until It Doesn't [Bloomberg]

Honeywell’s decision to spin off its aerospace and automation divisions marks a significant step in dismantling its broad conglomerate structure, reflecting mounting investor skepticism toward diversified industrial giants. The move, prompted partly by activist investor Elliott Investment Management, follows a broader trend of industrial breakups seen in companies like General Electric, Danaher, and DuPont. Despite Honeywell’s efforts to align its businesses around automation, aerospace, and energy transition themes, its disparate product mix—from cockpit controls to barcode scanners—failed to generate cohesive growth, leading to lagging stock performance compared to more focused rivals. This contrasts with Parker-Hannifin, which has pursued diversification through acquisitions, smoothing out earnings volatility and outperforming Honeywell with a 35% stock increase over the past year versus Honeywell’s 8%. While Honeywell’s separation will streamline operations, history suggests that partial breakups often lead to further divestitures, as seen with other industrial firms that split once the process began. This broader trend underscores growing investor preference for simplification over complexity, even in companies that don’t fit the traditional conglomerate mold. Firms like Becton Dickinson, Middleby, and MKS Instruments—each with seemingly logical business groupings—are now under pressure to break up further, often at the urging of activist investors. Becton Dickinson, for example, announced plans to separate its life sciences division following pressure from Starboard Value despite having already spun off its diabetes business in 2022. Similarly, Middleby is reassessing whether its residential oven and meat grinder units belong in the same division as its commercial-grade restaurant equipment. Meanwhile, MKS Instruments faces investor reluctance to embrace its broad semiconductor-related portfolio despite its strategy of maintaining a presence across multiple chipmaking subsystems to hedge against industry shifts. The current wave of corporate simplifications raises concerns that the pursuit of focus may sometimes prioritize financial engineering over long-term strategic value creation, highlighting a fundamental tension between market perception and operational reality.

US Solar Manufacturing Is Finally Thriving. Will Trump Derail It? [Canary Media]

The U.S. solar industry has reached a significant milestone. The annual production capacity for solar panels now exceeds 52 gigawatts (GW), up from 40 GW in late 2024, surpassing the Solar Energy Industries Association’s (SEIA) 2020 goal of 50 GW by 2030. However, the U.S. relies on imported solar cells, as domestic factories primarily assemble modules from foreign-made cells, wafers, and ingots. Companies have pledged 56 GW of solar-cell production capacity to close this gap, but these projects require substantially higher capital investment than module assembly. Cell manufacturing involves complex chemical processes requiring clean-room environments, costing around $130 million per GW—over four times the cost of panel assembly. While companies like Suniva and ES Foundry have begun small-scale domestic cell production, larger efforts, such as QCells’ 3.3 GW Georgia plant and Silfab Solar’s 1 GW South Carolina facility, are still under construction. The uncertainty surrounding President Trump’s executive order pausing funding from Biden-era climate laws has created hesitation among investors, particularly concerning the 45X manufacturing tax credit, which has been instrumental in securing loans for solar-cell factory construction. The 45X tax credit, introduced under the Inflation Reduction Act, provides financial incentives for domestic solar manufacturing by awarding payments per component produced. Companies without sufficient tax liabilities can sell these credits to generate cash, a crucial mechanism for financing new factories. Heliene, a Canadian solar manufacturer with a U.S. presence, leveraged 45X credits to secure $50 million. However, its planned $200 million solar-cell factory remains on hold until there is clarity on the future of tax incentives. Unlike corporate-backed firms like QCells, smaller solar manufacturers lack alternative funding sources, making tax-credit-based financing essential. Without assurance that these credits will remain intact, lenders are reluctant to finance the estimated $100 million-plus cost of solar-cell plants, further delaying investments. SEIA has launched a lobbying push, engaging with over 100 members of Congress to protect these credits, while some Republicans support them for their economic benefits. If the uncertainty persists or Congress rescinds the credits, planned cell factories—and the high-tech, well-paying manufacturing jobs they promise—could collapse, jeopardizing U.S. efforts to build a fully domestic solar supply chain.

Where Is Trump’s Tariff Strategy Going? [WSJ]

President Trump’s tariff strategy has escalated with a 25% tariff on all imported steel and aluminum, affecting key trading partners such as Canada, Mexico, and Brazil, alongside a 10% tariff on all Chinese imports. Trump has also proposed reciprocal tariffs, which would impose duties on imports based on those countries' tariffs on U.S. goods. This could significantly impact India, Brazil, Vietnam, Argentina, and developed economies like Japan and the European Union, particularly in agriculture and automotive exports. While Trump argues that tariffs will protect American manufacturing, reduce the trade deficit, and create jobs, many economists warn that they may increase U.S. consumers' prices, disrupt supply chains, and lead to retaliatory measures from affected countries. For example, China has already imposed 15% tariffs on U.S. coal and liquefied natural gas while raising duties on crude oil, agricultural machinery, and vehicles. Additionally, tariffs could raise production costs for American manufacturers, especially in industries reliant on imported parts, potentially leading to job cuts and profit margin squeezes. As tariffs expand, their impact on inflation, global supply chains, and trade relations will be closely watched, particularly as U.S. businesses and consumers brace for potential cost increases.

Research:

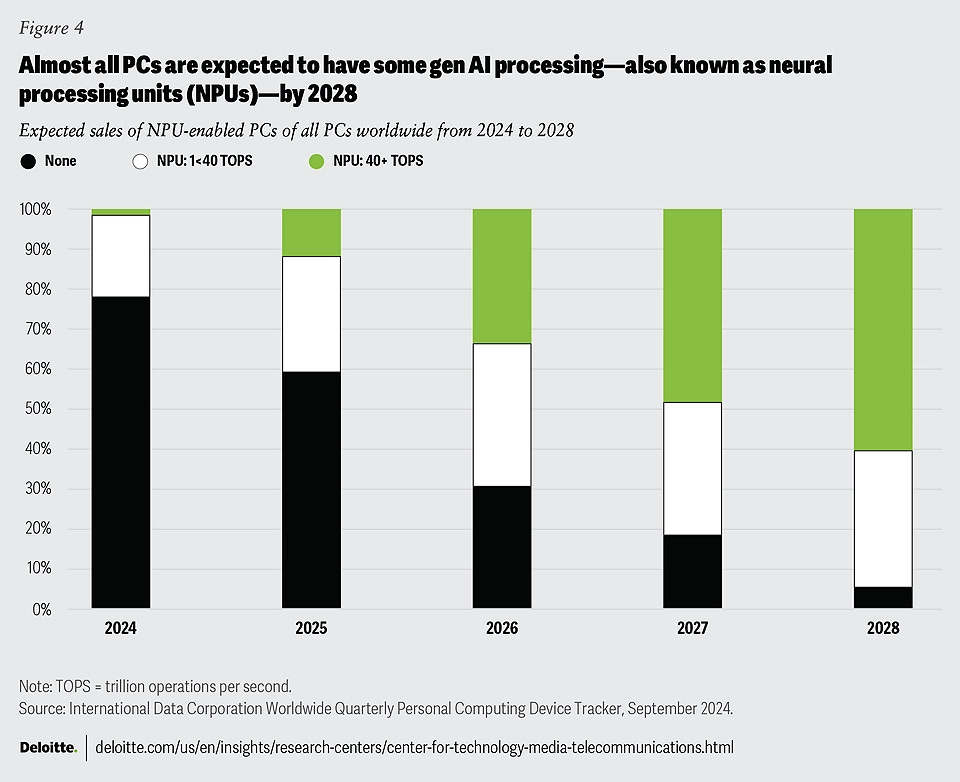

2025 Semiconductor Outlook [Deloitte]

The semiconductor industry experienced significant growth in 2024, with sales reaching $627 billion—exceeding earlier forecasts—and an expected 11% increase in 2025, pushing sales to $697 billion. The industry is on track to reach $1 trillion by 2030 with a required compound annual growth rate (CAGR) of 7.5%. The market capitalization of the top 10 semiconductor companies surged 93% year-over-year, reaching $6.5 trillion, primarily driven by demand for generative AI (Gen AI) chips. AI-related semiconductors accounted for over $125 billion in 2024—more than 20% of total chip sales—and are projected to exceed $150 billion in 2025. While Gen AI accelerators dominate revenue growth, they represent a small fraction of total wafer production, leading to lower overall capacity utilization. Despite a 19% increase in semiconductor revenues in 2024, silicon wafer shipments declined by 2.4%, though they are expected to rebound by 10% in 2025, driven by increasing demand for chiplets and advanced packaging. TSMC’s CoWoS advanced packaging capacity is set to grow from 35,000 wafers per month in 2024 to 90,000 wafers per month by 2026, reflecting a growing shift toward high-performance computing architectures.

Generative AI’s expansion influences multiple end markets, including PCs, smartphones, and enterprise edge computing. AI-powered PCs are projected to make up 50% of total PC sales in 2025, with the majority incorporating onboard neural processing units (NPUs). Smartphone sales, expected to reach 1.24 billion units in 2025, will see 30% of new devices featuring AI chips, though their per-unit semiconductor impact remains lower than that of PCs. AI chips in IoT devices remain early, but long-term demand could be substantial. The industry faces growing talent shortages, requiring over 100,000 skilled workers annually through 2030, while geopolitical tensions—including U.S. export restrictions and China’s curbs on critical materials—are reshaping semiconductor supply chains. The U.S. Chips Act and similar policies in Europe and Asia drive onshoring, though talent constraints and high capital costs pose challenges. The industry remains vulnerable to trade disputes, extreme weather events, and fluctuating demand, particularly in AI-driven segments. Despite these risks, semiconductor companies prioritize R&D, with expenditures rising from 45% of EBIT in 2015 to 52% in 2024. While 2025 looks strong, the industry’s cyclical nature raises uncertainties for 2026, requiring companies to strategically navigate investment, talent, and geopolitical risks to sustain growth.

Open Sourcing π0 [Physical Intelligence]

Physical Intelligence has released the π0 robotic foundation model as open-source through its OpenPi repository, enabling researchers and developers to fine-tune the model for various robotic tasks and platforms. π0 is a general-purpose robotic foundation model designed to control different robot types, such as single-arm, dual-arm, and mobile robots, and perform tasks like folding laundry, cleaning, and scooping objects. The open-source release includes code, model weights, fine-tuned checkpoints for widely available robotic platforms, such as ALOHA and DROID, and tools for real-world and simulated deployments. OpenPi aims to democratize robotic learning, allowing users to adapt and optimize π0 with 1 to 20 hours of fine-tuning data for their specific applications. The repository also includes a PyTorch port developed by Hugging Face, ensuring compatibility with different machine-learning frameworks. The team acknowledges that π0 was initially developed for their in-house robots and that adaptation success may vary across various platforms. However, early testing has demonstrated strong generalization in environments not seen in training data, particularly with the DROID Franka robotic arm and ALOHA dual-arm system. The OpenPi release provides several key models, including the π0 base model, optimized for fine-tuning, and the π0-FAST model, which improves language-following capabilities at a higher inference cost. Additionally, pre-trained checkpoints are available for specific tasks and platforms, such as DROID (general robotic control), ALOHA (dexterous manipulation), and Libero (benchmark tasks). While these fine-tuned models offer out-of-the-box demonstrations, their performance may depend on the robotic setup. Physical Intelligence sees OpenPi as a crucial step toward general-purpose robotic control, drawing parallels with the impact of open-source language and vision-language models in AI.

Podcasts/Video:

Palantir’s Vision for US Defense [Odd Lots]

Finance & Transactions 🏭💵

Venture Capital:

Apptronik - A company building Apollo, a humanoid robot whose tasks will include working in warehouses and manufacturing plants.

$350 million [Series A] - Led by B Capital & Capital Factory with participation from Google.

Desteia - A company building a comprehensive suite of tools to enhance supply chain visibility and optimize their logistics.

$8 million [Seed] - Led by Autotech Ventures, Nazca, & Village Global and joined by Foundamental, Bridge Latam, & Nido Ventures.

Saeki - A company building the first on-demand additive manufacturer for large parts with complex geometries

$6.7 million [Seed] - Led by Lightbird and joined by Founderful, 2100VC, & Danobat.

Trace.Space - A company building requirements management for software-defined hardware

$4 million [Seed] - Led by Cherry Ventures and joined by Outlast Fund, Nebular, Fiedler, & Change Ventures.

Planned Downtime 🏭🧑🔧

Close Encounter @ SNL 50